Data drives today’s business decision-making. Healthcare is no exception. Urgent care organizations and providers increasingly count on data and analytics to inform their practice, improve care, and lower costs, in an effort to deliver a value-based, patient-focused, and cost-effective urgent care experience. It’s not the future—it’s today.

Each quarter, we measure the metrics and drill down on the data to bring you relevant information specific to the dynamic urgent care industry. In our last issue of Urgent Care Quarterly, we looked at wait time trends and their impact on patient satisfaction. In our current issue, we look at urgent care reimbursement and the variable that affect it. We provide data today, so you can make better decisions about tomorrow.

Urgent Care Reimbursement Trends 2013-2016

An Analysis of Reimbursements Changes Over the Years

Revenue is the lifeblood of your urgent care business and reimbursement per visit is an important indicator of your clinic’s performance. Simply put, reimbursement per visit is one of the easiest things to watch to predict revenue and potential success. But many factors like front-desk efficiency, real-time insurance verification, accurate coding, complete documentation, payer contracts, and effective collection processes play a part in reimbursement per visit—and your success. Viewed through a wider lens that takes visit volume and other variables into account, this metric helps urgent cares assess their overall performance and future outlook.

Comparing your clinic’s average reimbursement per visit to that of competitors and industry leaders is the first step to creating a strategy for success. The second step is exploring the reasons your numbers are either higher or lower than the industry average, and making any necessary changes.

Our goal in this issue is to help you take the first step. We will explore 2013–2016 reimbursement trends for urgent cares both by region and nationally. We looked at urgent care-specific visits only, and didn’t include OccMed or Work Comp visits in our analysis. We’ll also dig into other factors that might affect average reimbursement per visit.

The data presented here is based solely on visits with closed claims, and the average reimbursement per visit is calculated by dividing total reimbursements (payments collected less any reversals or refunds) by visit count.

REIMBURSEMENT PER VISIT

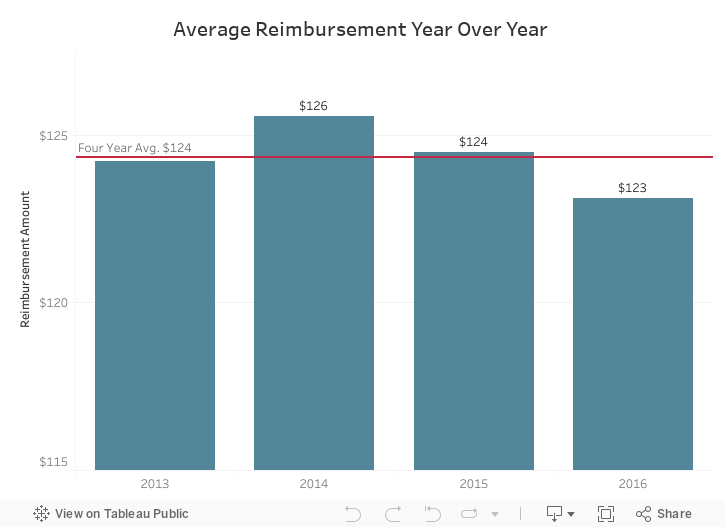

First, let’s take a look at reimbursement per visit over a four-year period to get a wide view of the trends in the urgent care industry. From 2013 to 2016, the average reimbursement per visit was $124, with a high of $126 in 2014, and a low of $123 in 2016—a three-dollar variance overall. [Figure A.]

FIGURE A.

On its own, the three-dollar variance seems somewhat insignificant, but even an incremental difference in reimbursement rate, when coupled with an increase in visit volume, can have a big impact on overall revenue for urgent care clinics.

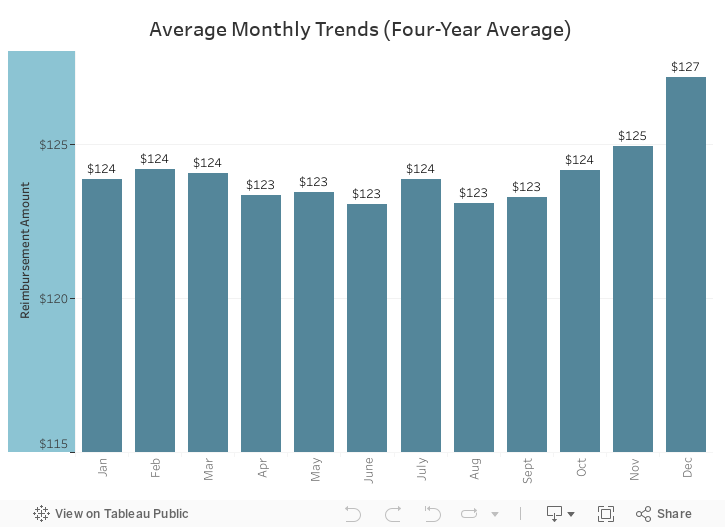

When we look at reimbursement per visit by month over that same period, the average for January through October is consistently between $123 and $124. Average reimbursement per visit then creeps up the last couple months of the year, with the highest month being December at $127 per visit. [Figure B.] This increase may reflect patients meeting their insurance deductible or higher acuity patients during flu season resulting in higher reimbursements for urgent care clinics.

FIGURE B.

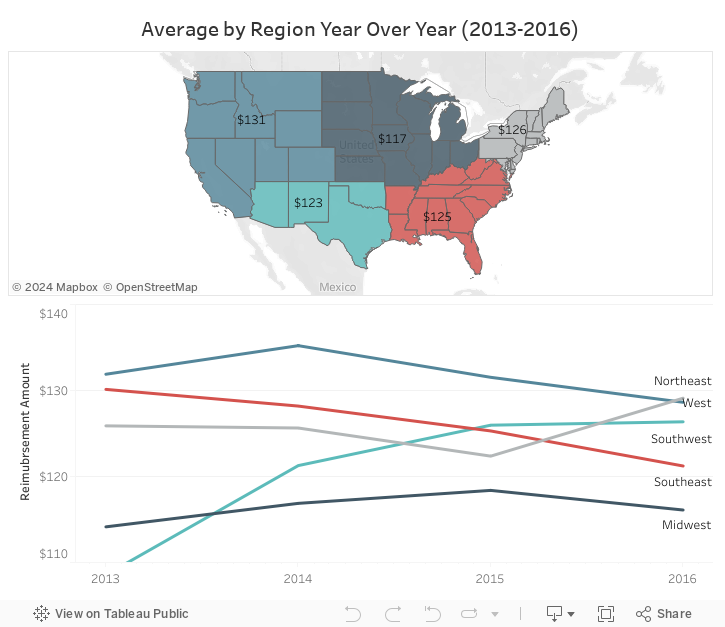

When we divide the country into regions, we can see a significant difference in average reimbursement based on location. Over the four-year period, the Midwest showed the lowest per-visit reimbursement at $117, and the West showed the highest at $131. [Figure D.] The widest variance between regions was $18 and occurred in 2013. The gap between the highest and lowest regions has been shrinking since that time. In 2016, that difference decreased to $13 per visit.

A few trends emerge as we look at individual regions, especially in the Southwest, where average reimbursements have risen from less than $110 per visit in 2013 to just over $125 in 2016. In the Southeast, average reimbursement per visit has fallen from about $130 in 2013 to just over $120 in 2016. Other regions have remained relatively consistent with little variation year over year. [Figure E.]

FIGURE D. AND E.

It’s important to remember that states retain some control over urgent care contractual rates, which might affect the overall average reimbursement in specific regions. The data suggests that as the industry continues to mature, we may see a stabilization of reimbursement rates year over year through better contract negotiations and payers understanding the value of urgent care. For urgent cares, strengthening operational processes and initiating smart cost-control measures will help clinics increase their profitability.

2016 REIMBURSEMENT PER VISIT CURVE

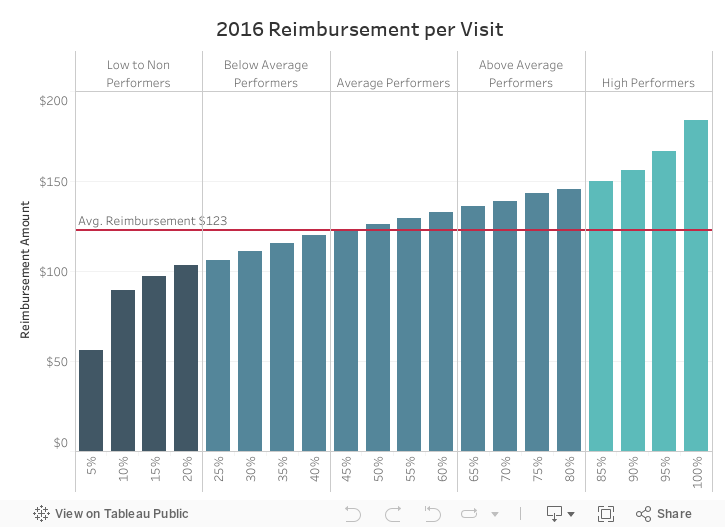

To provide more insight into how your reimbursement stacks up, we looked specifically at 2016. The average reimbursement of $123 is consistent with the four-year trend of $124 per visit. Clinics in the lowest 20 percent based on average reimbursement received $100 or less per visit, while clinics in the highest 20 percent received $150 or more per visit. [Figure F.]

FIGURE F.

These significant differences could be the result of a number of contributing factors. As we referenced earlier, regional differences affect reimbursement. But some other controllable variables might also affect these numbers, including proper coding and processing, collection percentages, and payer contracts. Also, new clinics may receive higher reimbursements for the short-term as they have more new, versus established, patients. More than anything, this data empowers clinics to evaluate their own practices and procedures to find areas for improvement to boost performance.

INSURANCE VERSUS PATIENT REIMBURSEMENT YEAR OVER YEAR

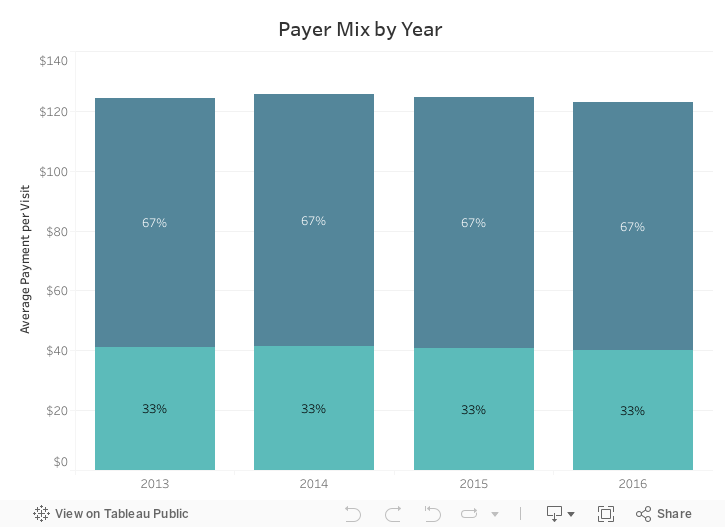

With an increased movement toward high-deductible insurance plans resulting in greater patient responsibility, we were interested in looking at what percent of reimbursements were made by insurance payers versus individual patients. Somewhat surprisingly, over the four-year period from 2013 to 2016, 33 percent of total payments were made by patients and 67 percent were made by insurance payers consistently, with virtually no variance year over year. [Figure G.]

FIGURE G.

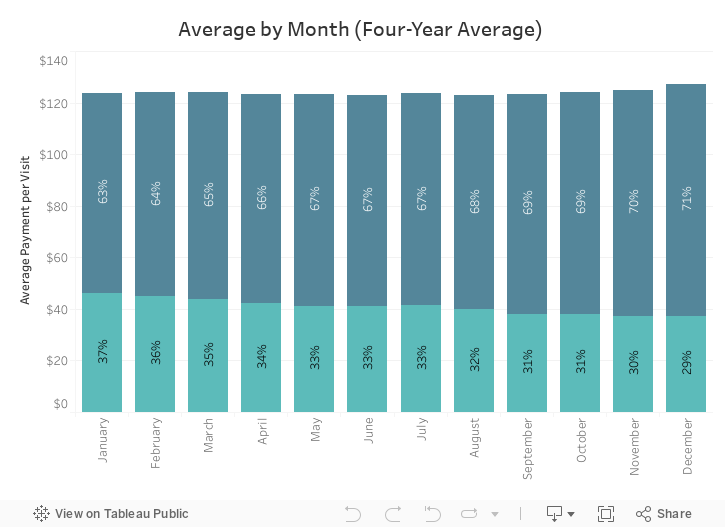

When looking at the reimbursement per visit mix monthly during 2016, the percentage paid by insurance payers increased from 63 percent in January to 71 percent in December, while patient percentage inversely decreased. [Figure H.] This can likely be attributed to patients meeting insurance deductibles toward the end of the year.

FIGURE H.

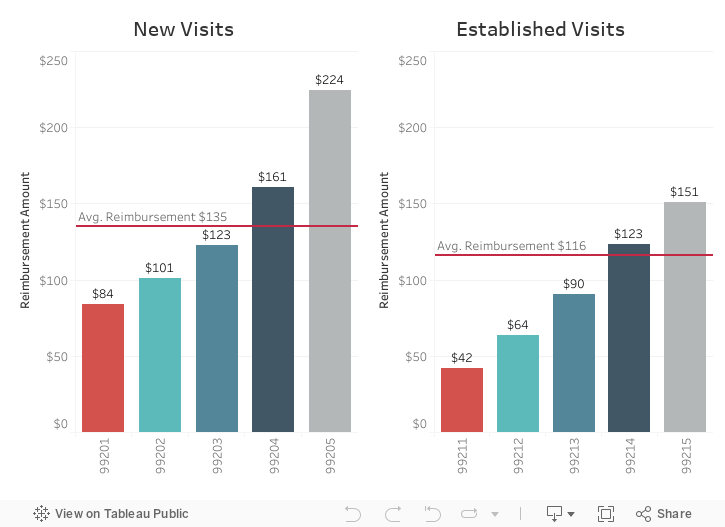

REIMBURSEMENT PER VISIT BY E/M CODE

As expected, the four-year average reimbursement per visit for new patients is higher than reimbursement for established patients at every E/M code level. When we look at all E/M codes combined, the average reimbursement for new patients is $135 versus $116 for established patients. [Figure I.]

FIGURE I

In response to this information, it’s a good idea to increase your marketing efforts in two specific areas:

THE EFFECT OF FRONT DESK COLLECTIONS

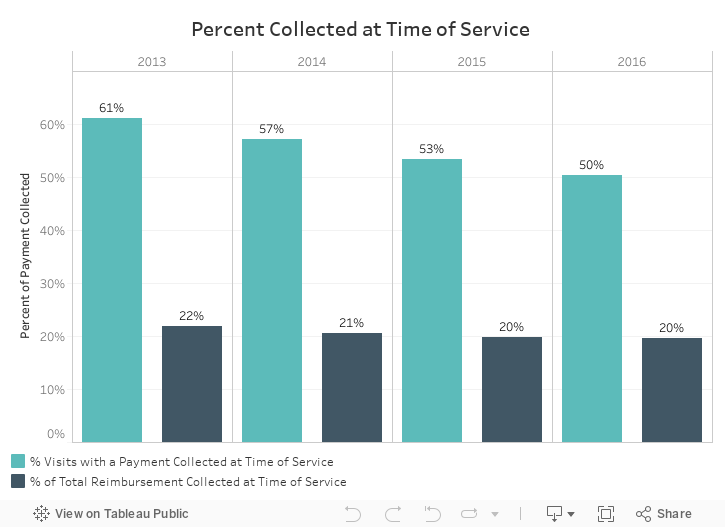

Your urgent care front desk is ground zero for ensuring timely and accurate reimbursement for urgent care services. Everything from asking for payment to making sure information is accurate is key to healthy reimbursement. Our research indicates that in 2016, a payment was collected at the front desk only half the time, down from 61 percent of the time in 2013. In addition, the percent of total reimbursement collected at the front desk has decreased, from 22 to 20 percent, over the four-year period from 2013–2016. [Figure J.] The result is approximately 80 percent of reimbursement remains to be collected from payers and patients when the patient is not in the clinic.

FIGURE J.

Once the patient leaves the office, more effort and staff hours are needed to complete the revenue cycle, which costs your clinic money. Claims could be denied by a payer for ineligibility, inaccurate patient registration, complex coding or contract terms, and even a reduction in covered benefits. All these things create hiccups in the A/R process, which is why collecting a greater percentage of payments at the front desk is so important.

Keeping payments flowing should be one of the main priorities of everyone at your clinic, beginning with the front desk staff. A large percentage of your revenue can (and should) be collected at the front desk, but not everyone is cut out for the job. Our experienced RCM team has found that very few people are naturally good at asking for money.

Your entire staff must be committed to accuracy and timely completion of charts to improve the odds of timely reimbursement from all payers.

We would love to see the downward trend of collecting at the front desk reversed because we believe that when more money is collected at the time of visit, the result is better, easier collections. To reverse this trend, utilize software that estimates patient responsibility at the end of the visit, ask for payment, and get a card-on-file so that collections happen seamlessly.

THE TAKEAWAY

Accurate and timely reimbursement is one of the main components to urgent care success. And while it’s impossible to predict the future of healthcare and the direction of the insurance industry, making adjustments at the clinic level is essential to riding out the ups and downs of the business.

The only way to make significant improvements is to get better at collecting for the services offered, leveraging technology to ensure efficient and effective revenue cycle management, and controlling other costs that affect overall revenue.

Have you audited your front desk protocols to be sure you’re collecting as much money as possible at the time of the patient visit? Are you managing your revenue cycle using all the tools and technology available? Are you using data to uncover issues that directly affect your reimbursement?

At DocuTAP, our goal has always been to provide a better urgent care experience. It starts with effective software solutions, but really means becoming a trusted business partner with our customers. By collecting and sharing urgent care data, we further our goal and the goals of urgent care clinics nationwide—for a smarter, stronger, and more robust industry.