In our last issue, we explored ICD-10, CPT, and E/M coding trends from 2013-2017, as they relate to urgent care. In this issue, we turn our focus to one of the most popular service lines in urgent care—occupational medicine. We hope the data provided in this issue will give you an overview of how offering employer services can affect an urgent care practice, and the industry as a whole. Most importantly, you’ll see real data from real clinics to help you make smart choices about OccMed and your practice.

Occupational Medicine Trends 2013-2017

If you offer occupational medicine (OccMed) and other employer services at your urgent care clinics, you’re not alone. A majority of urgent cares offer some level of OccMed to their patients and regional employers. Some urgent cares are all in, offering a wide range of employer-paid healthcare services. Others handle it on a much smaller scale and barely promote it as an available service line. Chances are you’re already serving some of the occupational medicine needs of patients and their employers.

Although we generally think of OccMed as pre-employment screenings, drug tests, and workers’ compensation, its definition continues to develop and expand as urgent cares provide more services to employers such as physical therapy for injured workers, corporate wellness programs, and even travel medicine for employees who regularly visit foreign countries.

There are a couple of common theories about why it makes sense to offer employer services. First, scheduled OccMed visits and walk-in workers’ comp visits can help balance patient visit volume throughout the year. Secondly, it can help generate new business as workers who come in for employer services return to the same clinic when they need urgent care—if they had a positive experience.

In this issue, we’ll explore employer services trends over the last five years as they relate to urgent care and find out if these theories hold true. First, we’ll look at the data from a broad perspective, then narrow the scope of our inquiry and dive deeper to provide greater insight into what these trends mean for on-demand healthcare providers.

Our Methodology

In order to provide meaningful data as it relates to the industry as a whole, the first part of this report includes data from urgent care clinics that are using or have used DocuTAP during the five-year period from 2013-2017, whether or not they provide employer services. As we get deeper into the report, we will use data from only the clinics that provide some level of employer services—OccMed, workers’ comp, or both—excluding those clinics that do not.

For the purposes of this report, we define OccMed visits as those in which an OccMed payer (employer) has been selected in the EMR/PM. Workers’ compensation visits are those identified as employment-related with a case ID number and a named workers’ comp insurer; employer services include both OccMed and workers’ comp. Urgent care visits are those that do not include any employer services.

Note: To better explore the data, we have defined five cohorts based on the percentage of employer services performed based on total visits: 0–5 percent; 6–10 percent; 11–15 percent; 16–20 percent; and 21+ percent (rounded to the nearest percent).

Figures E, F, G, and K include data only from clinics that perform some level of employer services.

The Impact of OccMed on the Industry

Let’s start with a look at the big picture. How much of the urgent care industry provides employer services in addition to urgent care services? And what do the numbers look like?

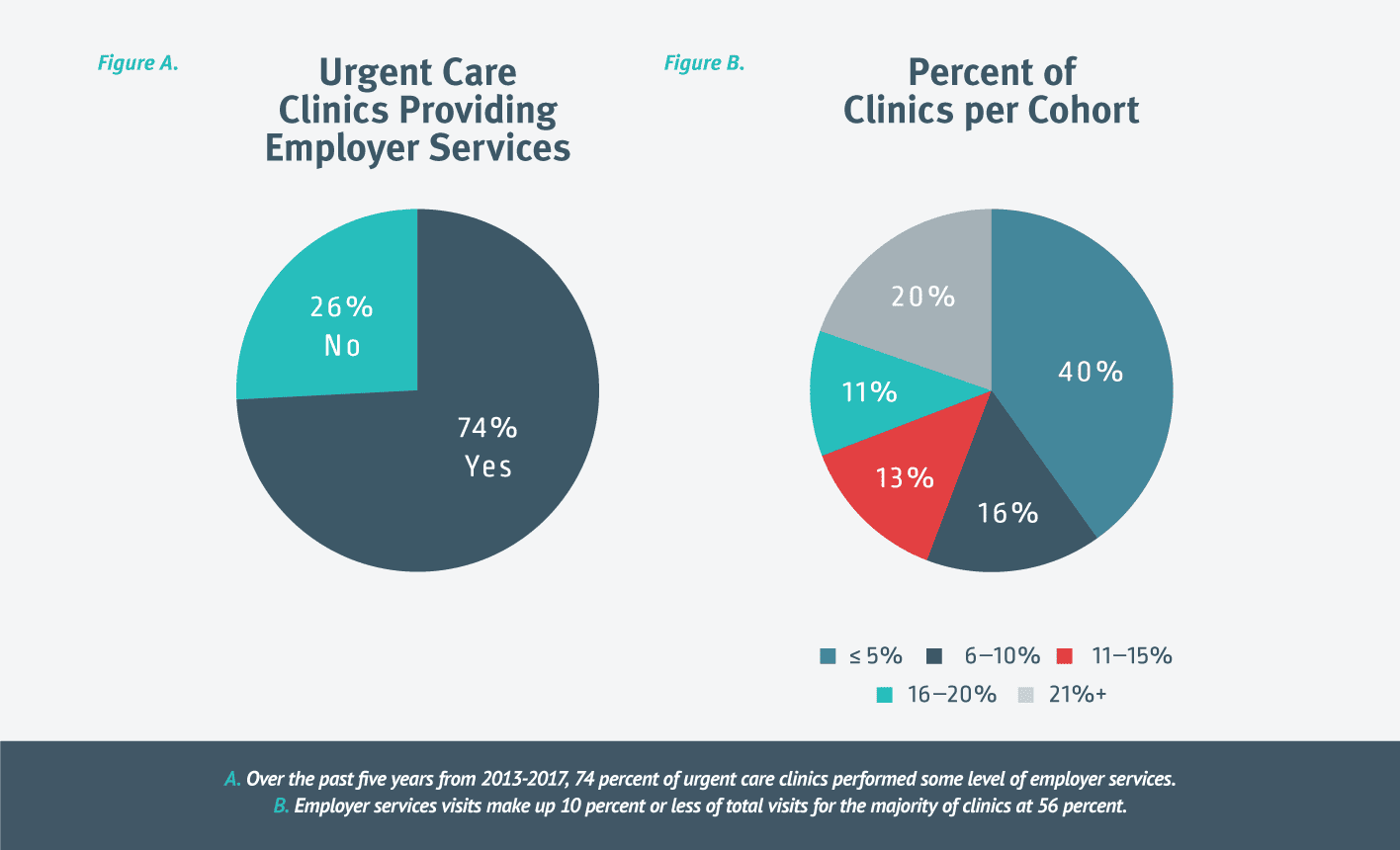

As you may have guessed, the overwhelming majority of urgent cares provide some level of employer services. Over the past five years, 74 percent of clinics conducted at least some OccMed or workers’ comp visits. [Figure A.] As more urgent cares explore the opportunities available through ancillary service lines, some clinics have made a bigger commitment than others.

When we look only at urgent care clinics that provide at least some employer services, employer services visits make up 10 percent or less of total visits for the majority of clinics (56 percent). Surprisingly, 20 percent of clinics have employer services account for 21 percent or more of their visits. [Figure B.]

Employer Services Impact on Visit Volume

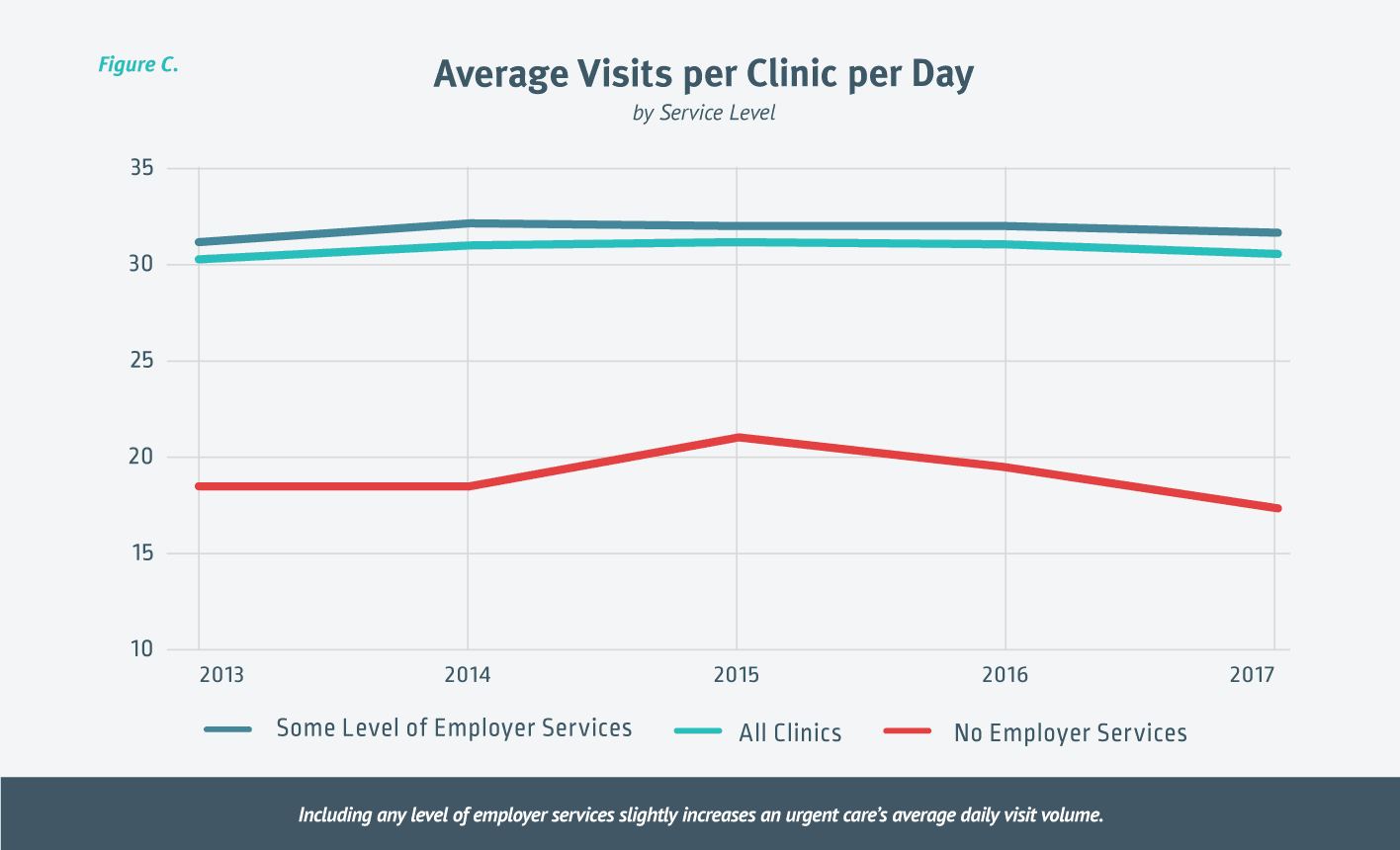

Including any level of employer services will increase an urgent care clinic’s average visits per day. When we look at the data across all clinics over the last five years, the average visits per clinic per day was approximately 31. Looking at the clinics that perform some level of employer services, the average visits per clinic per day jumps slightly to 32, while clinics not providing employer services had an average of 19 visits per day. When we looked for reasons clinics that performed no employer services had fewer visit per day, we didn’t find a specific reason, but we did find that these clinics are generally lower performers when it comes to visit volume. [Figure C.]

When we look at the overall impact of employer services on the urgent care industry, the data indicates that these visits represent a relatively small percent of all urgent care visits. But the number of visits is steadily growing. In 2013, employer services accounted for eight percent of all urgent care visits. That number grew to 14 percent in 2017. While the average number of urgent care-specific visits per day remained mostly consistent over five years, OccMed visits nearly doubled from 1.79 to 3.44. [Figure D.]

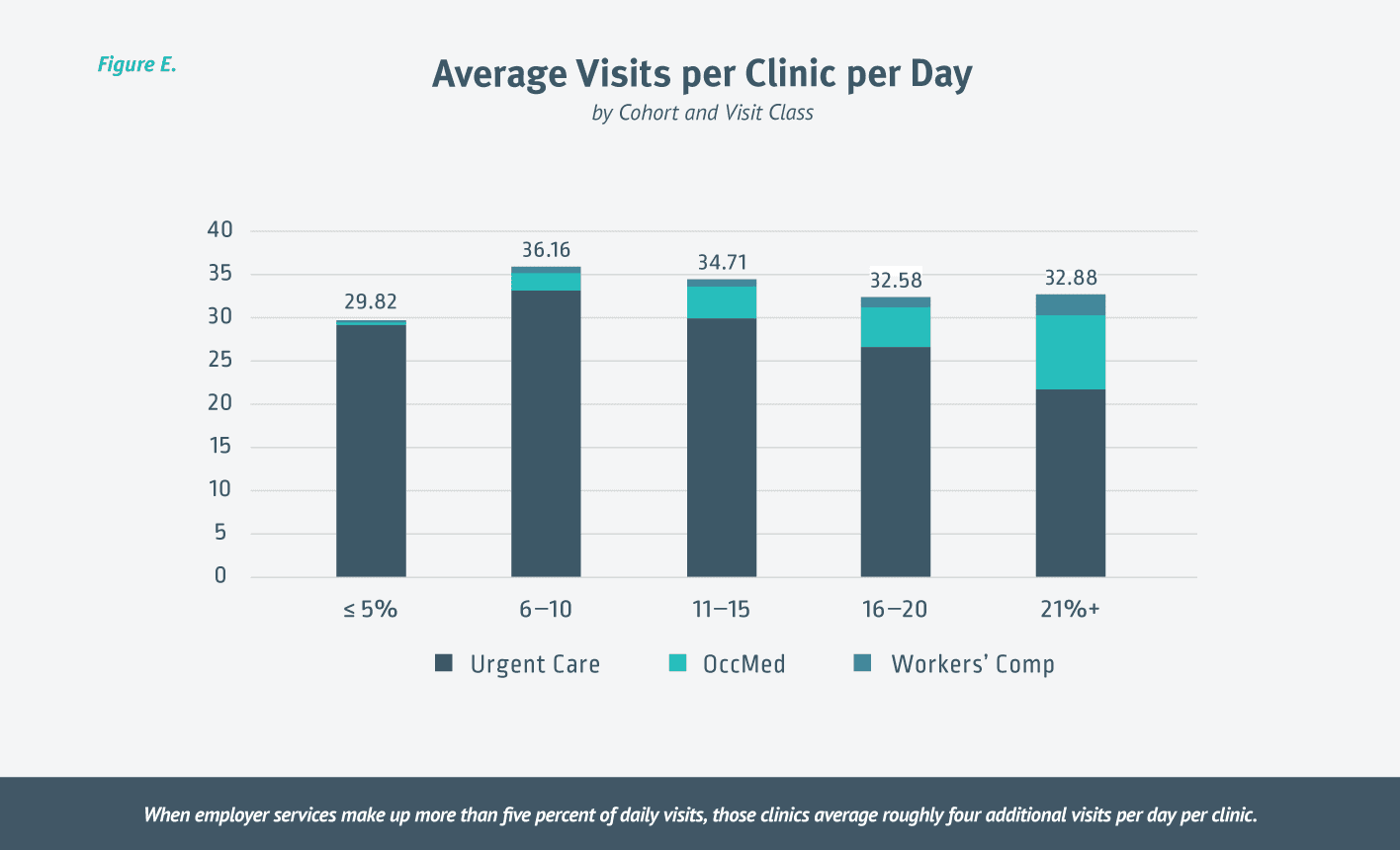

When we break down visits per day by cohort and visit class we see that when employer services make up more than five percent of daily visits, those clinics average roughly four additional visits per day per clinic. The average number of visits was highest—just over 36 visits—for clinics in which employer services accounted for six to 10 percent of all visits. [Figure E.]

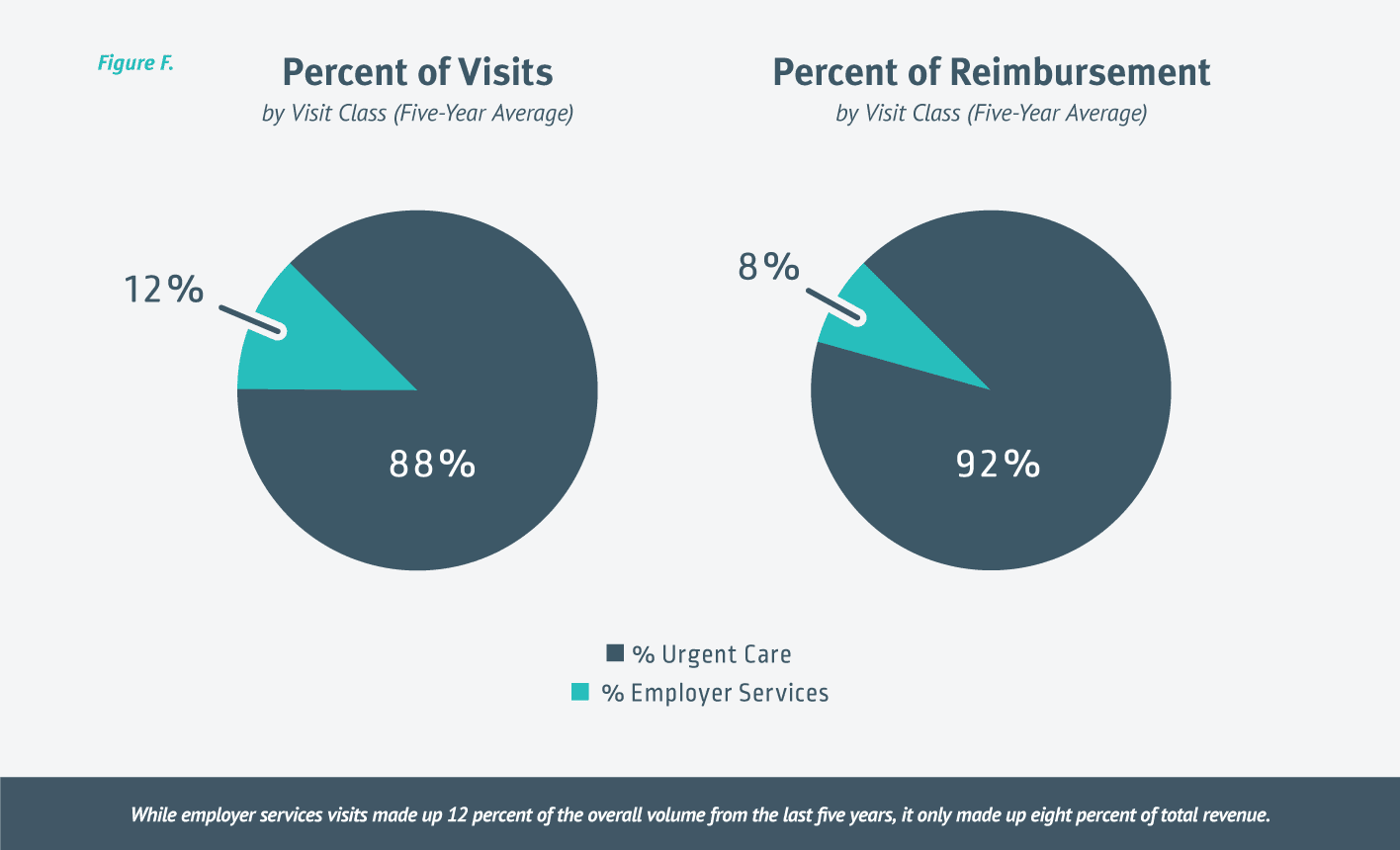

While employer services visits made up 12 percent of the overall volume from the last five years, it only made up eight percent of total revenue. [Figure F.]

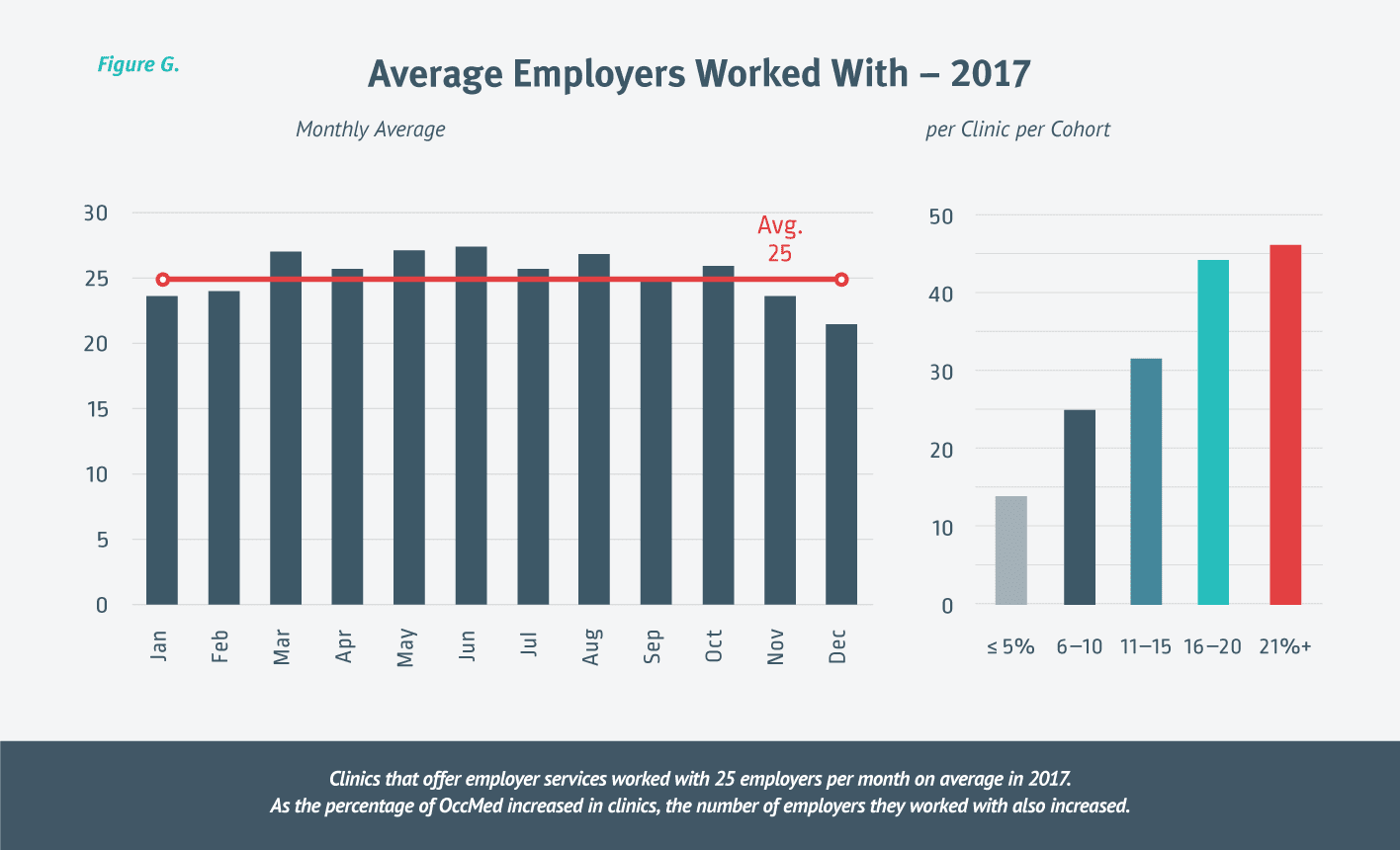

How Many Employers Do Urgent Care Clinics Work With?

We thought it would be interesting to see just how many companies urgent care clinics work with and how that number correlates to the percent of visits attributed to employer services.

Looking only at urgent care clinics that provided some level of employer services for 2017, research shows that the average urgent care clinic worked with approximately 25 unique employers each month, and about 77 total employers throughout the year. As expected, the employers overlap month over month due to contractual agreements.

As the percentage of OccMed services rendered increases, it’s not surprising that the overall number of employers they work with also increases. [Figure G.]

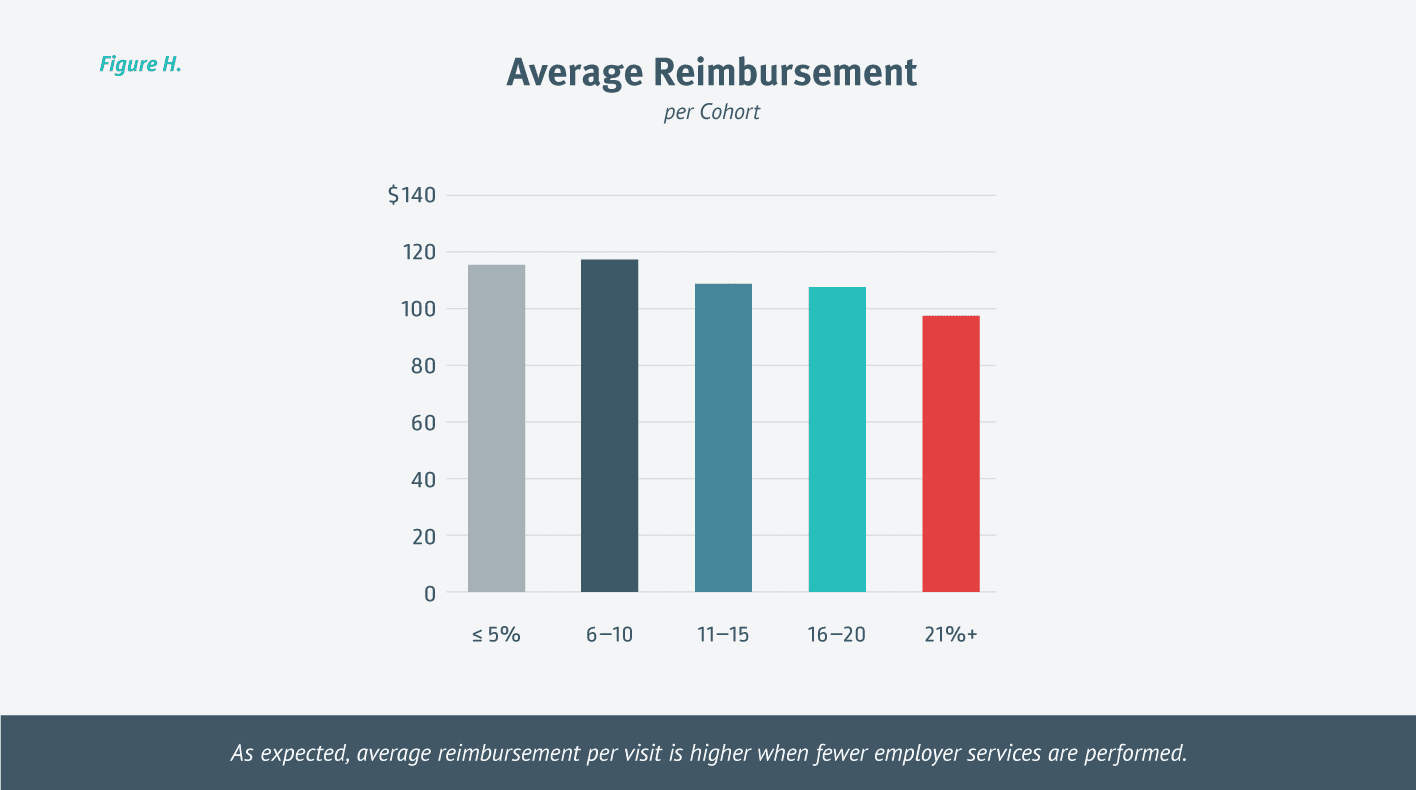

How is Reimbursement Affected by Offering Employer Services?

While reimbursement for urgent care visits is generally higher than reimbursement for OccMed, reimbursement for workers’ comp visits is often higher than for urgent care visits. Since clinics that are performing employer services perform more OccMed than workers’ comp visits, it makes sense that from 2013-2017 clinics saw the highest reimbursement per visit when they provided 10 percent or less of employer services. [Figure H.]

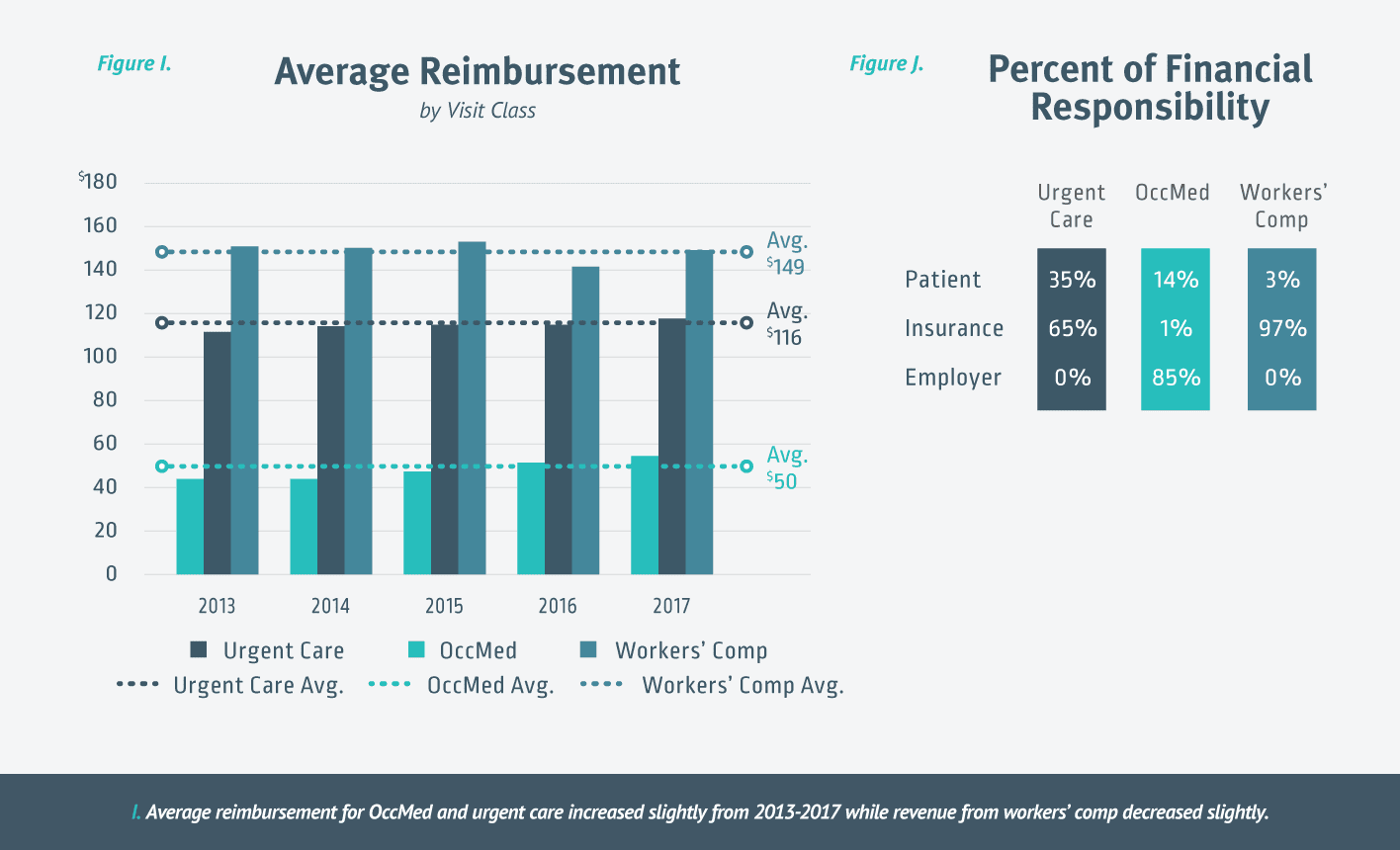

The average reimbursement per OccMed visit is less than half the reimbursement for urgent care visits and about 1/3 the reimbursement for a workers’ comp visits. Average reimbursement for OccMed and urgent care visits increased slightly from 2013-2017 while revenue from workers’ comp decreased slightly. [Figure I.]

Who is Paying for Services Rendered?

Whether it’s an urgent care, OccMed, or workers’ comp visit significantly impacts who pays for that visit. On average, 65 percent of an urgent care visit is paid by insurance while insurers pay 97 percent of a workers’ comp visit. OccMed visits, on the other hand, are almost entirely reimbursed by employers.

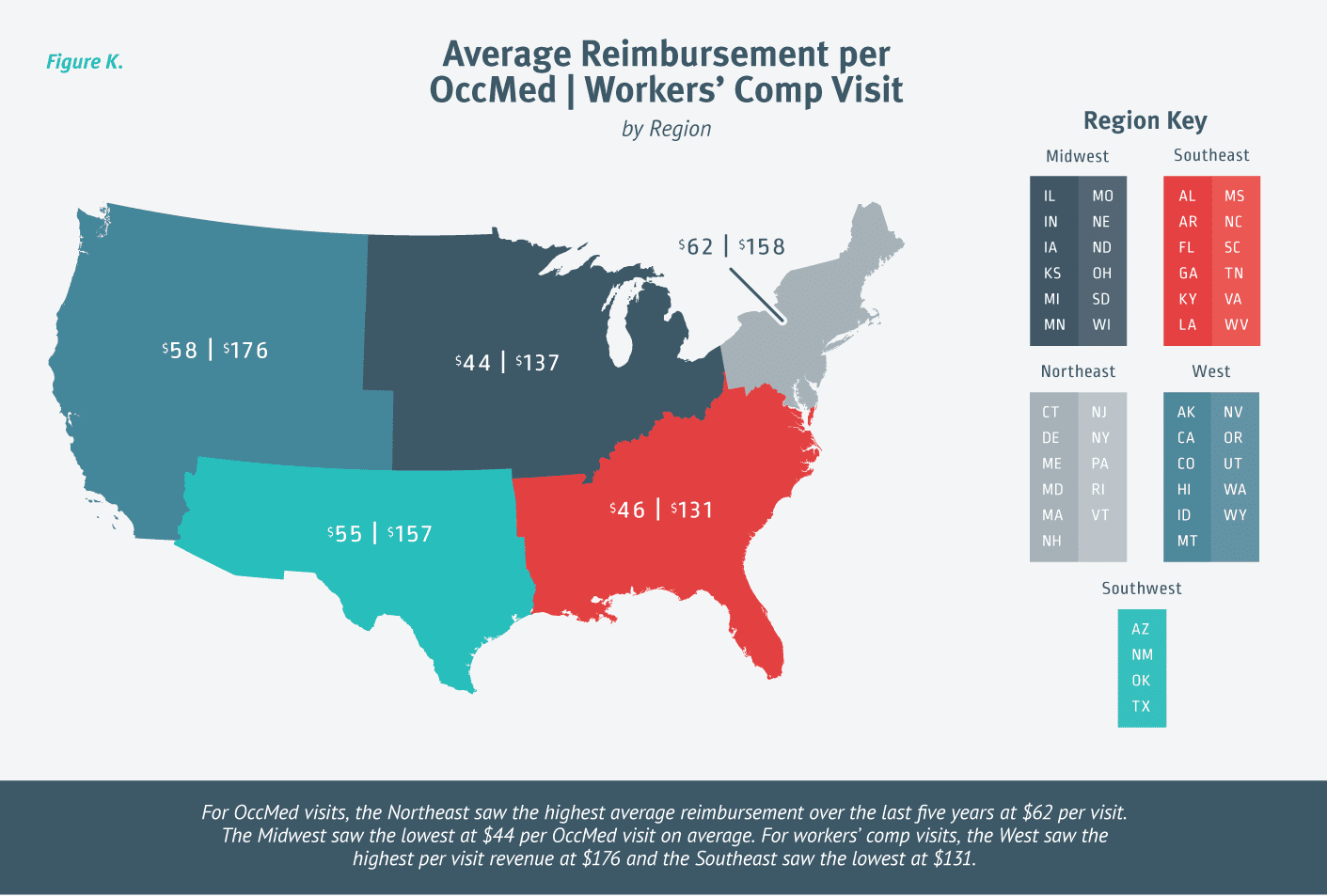

Regional OccMed Reimbursement Trends

When it comes to urgent care, location always makes a difference. This holds true for employer services as well.

For OccMed visits, the Northeast saw the highest average reimbursement over the last five years at $62 per visit. The Midwest saw the lowest at $44 per OccMed visit on average. [Figure J.]

There’s a larger variance in regional workers’ comp reimbursement as the reimbursement is much higher than OccMed. The West saw the highest per visit revenue at $176 and the Southeast saw the lowest at $131. [Figure K.]

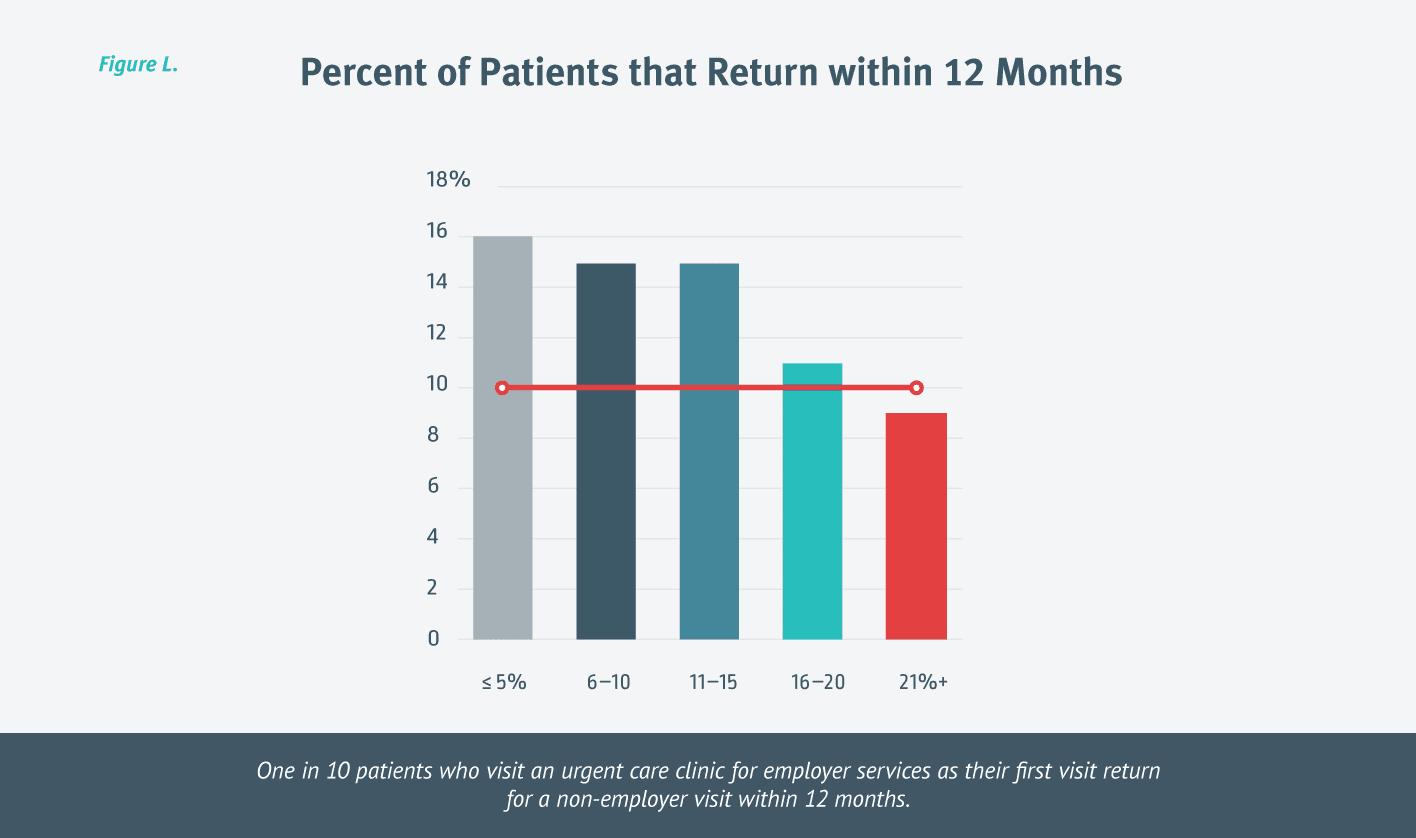

Do OccMed Visits Drive Urgent Care Visits?

The answer is yes. One in 10 patients who visit an urgent care clinic for employer services as their first visit return for a non-employer visit within 12 months. [Figure L.]

Interestingly, the more OccMed a clinic performed, the less likely it was for the patient to return for an urgent care visit within 12 months. This could be due to a number of factors, from how the clinic is marketed or viewed by the patient to the demographic or type of patients being seen.

The Takeaway

According to U.S. Bureau of Labor Statistics, there were 892,270 occupational injuries and illnesses in 2016 that resulted in days away from work in private industry. Companies have a need for expert workplace health services to help manage not only workplace injuries, but to help them maintain a healthy workforce.

Urgent care clinics are a natural solution to delivering these services because of their commitment to on-demand healthcare, extended hours, quick door-to-door time, and easy accessibility. For so many reasons, employer services continue to be a good option for urgent cares trying to supplement their volume and revenue while also attracting new patients.

At Experity, our goal has always been to provide a better urgent care experience. We stand behind our software and services, but more importantly, are committed to urgent care clinics as a trusted business partner. By collecting and sharing urgent care data, we further our goal and support the goals of urgent care clinics nationwide—providing a better urgent care experience for patients, providers, and everyone in between.