Skip to Main Content

Close Search Box

Search for:

Search

Urgent Care Connect

Urgent Care Resources

Urgent Care Software Suite

Search

Get Support

Login

Experity EMR/PM

DocuTAP EMR/PM

Clockwise Patient Engagement

Calibrater Patient Engagement

Experity Connected

Business Intelligence

EMR & PM

Teleradiology

Patient Engagement

Revenue Cycle Management

Get Started

Urgent Care Connect

Urgent Care Resources

Urgent Care Software Suite

Get Started

Resources

/

Research

Urgent care data and trends

Urgent Care Revenue Cycle Trends

Read this UCQ issue to see the latest visit trends and explore the biggest factors affecting your revenue cycle in...

Urgent Care Success Factors

Read this UCQ issue to see the latest visit trends and explore the threads common to thriving, growth-minded urgent care...

Urgent Care Industry Benchmarking

In the wake of the pandemic, we see an urgent care market today that looks very different than it did...

The Effects of Low-Acuity Patient Visits on Urgent Care Revenue

Explore how low-acuity visits are leading to a decrease in urgent care reimbursement and affecting your profitability. Get expert advice...

Driving Urgent Care Visit Volume with COVID-19 Test & Treat

Our partnership with more than 5,700 urgent care clinics in the U.S. helps Experity provide reliable, relevant data to help...

Learning from the Past; Forecasting the Future

Read this UCQ issue to access the visit volume metrics, data, and trends that continue to redefine our business, and...

Urgent Care Visit Volume Trends

In this issue of Urgent Care Quarterly, we’ll explore the factors that have an impact on visit volume and revenue...

How Did 2020 Impact Urgent Care? – Infographic

This summer, we conducted a survey to gain insights into the impact 2020 had on urgent care and where the...

The Effect of COVID-19 on Reimbursement in 2020

During 2020, the urgent care industry experienced evolutionary change as COVID-19 swept across the country. While urgent care providers were...

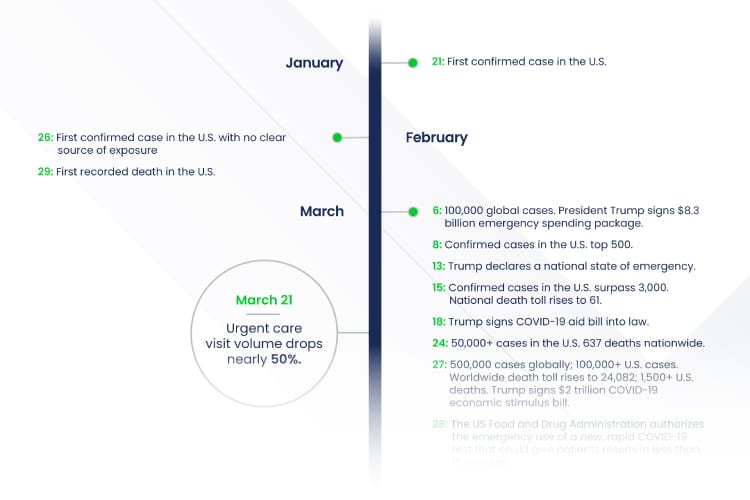

COVID-19 Pandemic 2020 Timeline

2020 is year that will go down in the history of global health. From January 21, when the first case...

The COVID-19 Pandemic Issue

In this issue of the Urgent Care Quarterly, we explore this public health emergency and the response of the urgent...

An Analysis of the Impact of Urgent Care Radiology

As on-demand healthcare becomes an increasingly important component of healthcare in America, urgent care organizations must continue to observe the...

×